Publishing > Malfeasance 101 > CPA Malfeasance - 2021

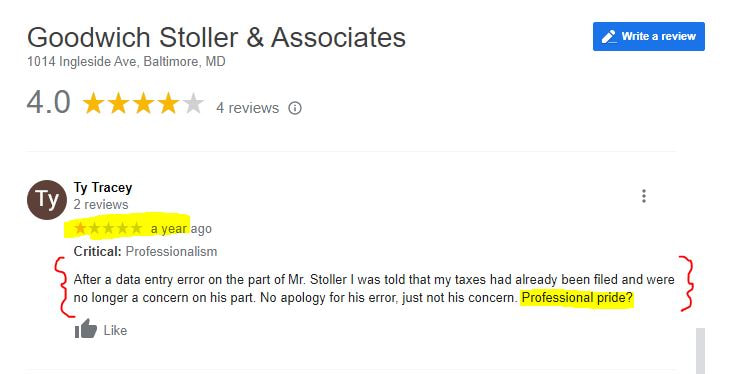

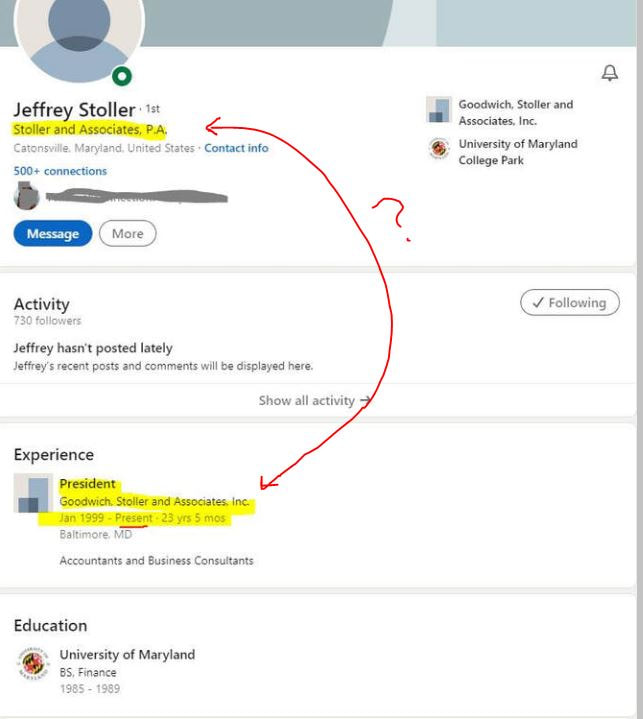

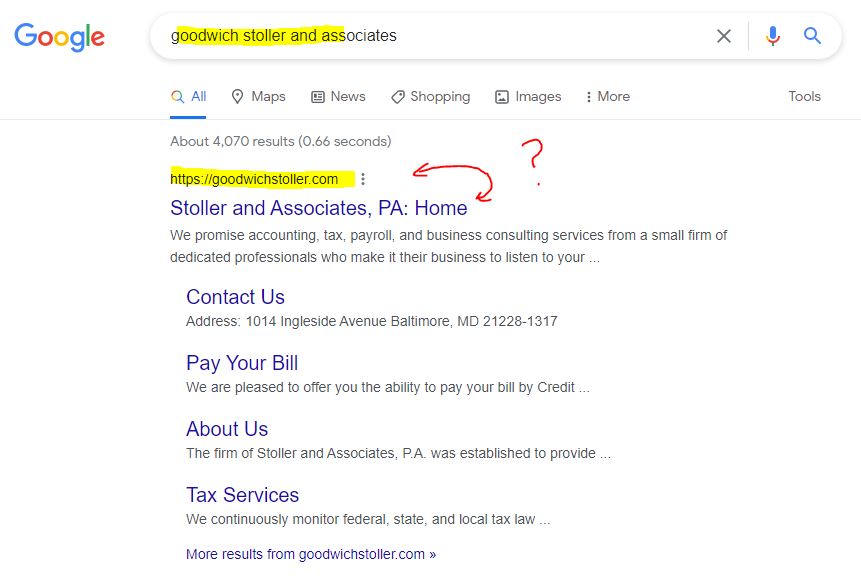

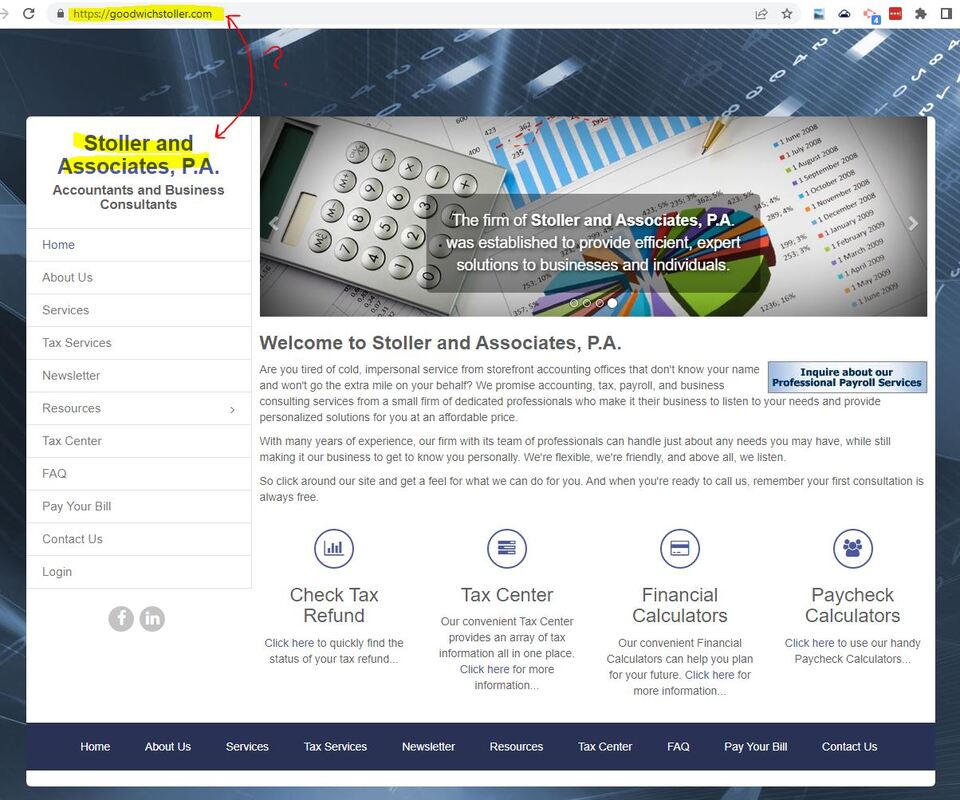

2022/09/22 - Maryland CPA Review Board - Notice of Systemic Problems and specific problems related to an Individual Complaint ( view )

I will likely publish the full complaint and the CPAs response to the board as well, but that would be after resolution is achieved on this outstanding matter.

-------------------------------------------------------

To the surprise of many, a Certified Public Accountant (CPA) may only provide ONE pivotal role for Self-Employed individuals in a way no other related Professional can do at this time.

Other professionals including Bookkeepers, Enrolled Agents (for Tax Filing), Accounting Professionals who are not CPA's, and Tax Attorneys can often time's provide services that fill many of the roles played by CPAs but they can't do one thing.

When a Small Business Person applies for a Mortgage the bank almost always asks for a "Letter from your CPA verifying Self Employment". In many ways it's a bit of an "odd request".

I will likely publish the full complaint and the CPAs response to the board as well, but that would be after resolution is achieved on this outstanding matter.

-------------------------------------------------------

To the surprise of many, a Certified Public Accountant (CPA) may only provide ONE pivotal role for Self-Employed individuals in a way no other related Professional can do at this time.

Other professionals including Bookkeepers, Enrolled Agents (for Tax Filing), Accounting Professionals who are not CPA's, and Tax Attorneys can often time's provide services that fill many of the roles played by CPAs but they can't do one thing.

When a Small Business Person applies for a Mortgage the bank almost always asks for a "Letter from your CPA verifying Self Employment". In many ways it's a bit of an "odd request".

- First, there is an assumption that you use a CPA for Taxes when that is not remotely needed for many self employed people. If you don't you are generally fine with every other aspect of life EXCEPT when you go to apply for a loan, and if you don't have the name of a CPA on your tax returns at that time, you are starting off one step further down the qualification ladder. In such case, you may be asked to get an Attestation Letters from a CPA related to the details in your bookkeeping and tax filing, which would be a larger request than the one referenced above. I've worked with a CPA since 2000 or so, and I started doing back then because I learned about the need for support back then the hard way.

- Second, given everything about a self-employed's income is found on a Tax Return which was signed by a CPA, why on earth would they need such a letter? It's almost as if they believe 1) a CPA might know more about your background than what is shown on your tax returns which he/she prepared (which might be tax fraud related), and 2) the request seems to be a probe to see if they'll disclose it.

- Third, the question often avoids seeking an inquiry into who did the bookkeeping for the records and the level of service the CPA provided for Tax Preparation. There seems to be an assumption made that a "reasonable amount of due diligence" was provided by the CPA during tax preparation, which in fact should have happened, but there's a lot of implied trust in the entire system that could be fully holey if folks wanted it to be that way.